Kraken Becomes First Crypto Firm Approved for Federal Reserve Master Account

The approval comes more than five years after Kraken filed an application with the Kansas City Fed in October 2020

Welcome to the Wednesday edition of the Crypto In America newsletter!

What you’ll read: Kraken makes history by securing access to the Federal Reserve; Coinbase CEO visits the White House; this week’s top stories; and SOMA.finance joins the podcast.

Kraken, the U.S.’s second-largest crypto exchange, has pulled off something no other crypto firm has managed to: secured coveted access to the Federal Reserve.

The exchange said on Wednesday that its Wyoming-based banking arm has been approved for a Federal Reserve master account by the Kansas City Fed, marking the first time a crypto-native company has gained direct, albeit limited, access to the Fed’s payments system. The approval comes more than five years after Kraken filed its application with the Kansas City Fed in October 2020.

The account gives Kraken a direct line into the Fed’s payments rails, but not full banking powers. Under the limited-purpose, or “skinny,” master account framework floated by Fed Governor Christopher Waller, the firm can hold reserves and settle in central bank money, but it cannot lend, access the Fed’s discount window, or operate as a traditional commercial bank.

Governor Waller is seeking to finalize his skinny master account proposal by the end of this year. The Kraken approval, sources close to the process tell Crypto In America, is designed as a “pilot” program to trial the skinny master account concept, which is in line with payments-only accounts provided by central banks in the United Kingdom, the European Union and Switzerland.

“This milestone marks the convergence of crypto infrastructure and sovereign financial rails,” said Kraken co-CEO Arjun Sethi in a blog post. “With a Federal Reserve master account, we can operate not as a peripheral participant in the U.S. banking system, but as a directly connected financial institution.”

The decision marks a historic shift for an industry long shut out of the traditional banking system, and signals a softening of tone at the Fed, which had previously adopted a more hawkish stance towards crypto regulation under the prior administration.

It also implies that the Fed believes Kraken has sufficient anti-money laundering and sanctions compliance practices in place to curb illicit finance risk, and that Wyoming’s regulatory framework for special purpose depository institutions is in line with Federal banking standards.

Wyoming Governor Mark Gordon and Senator Cynthia Lummis (R-WY) hailed the approval as a milestone for the state’s progressive crypto framework. Lummis dubbed it a “watershed moment” for the industry, and Gordon described it as “good news for our state banks and special purpose depository institutions.”

The move could spark a surge of Fed master account applications from other crypto firms. On the horizon: Wyoming’s Custodia Bank, which has been chasing access nearly as long as Kraken and has been engaged in litigation against the Fed since 2022. Anchorage Digital, an OCC-regulated trust bank, and Ripple, through its trust company Standard Custody & Trust, have also applied for master accounts, much to the chagrin of many traditional banking outfits.

During last month’s comment period, banking trade groups cautioned that skinny master accounts could pose risks to banking system safety because crypto is less tightly regulated.

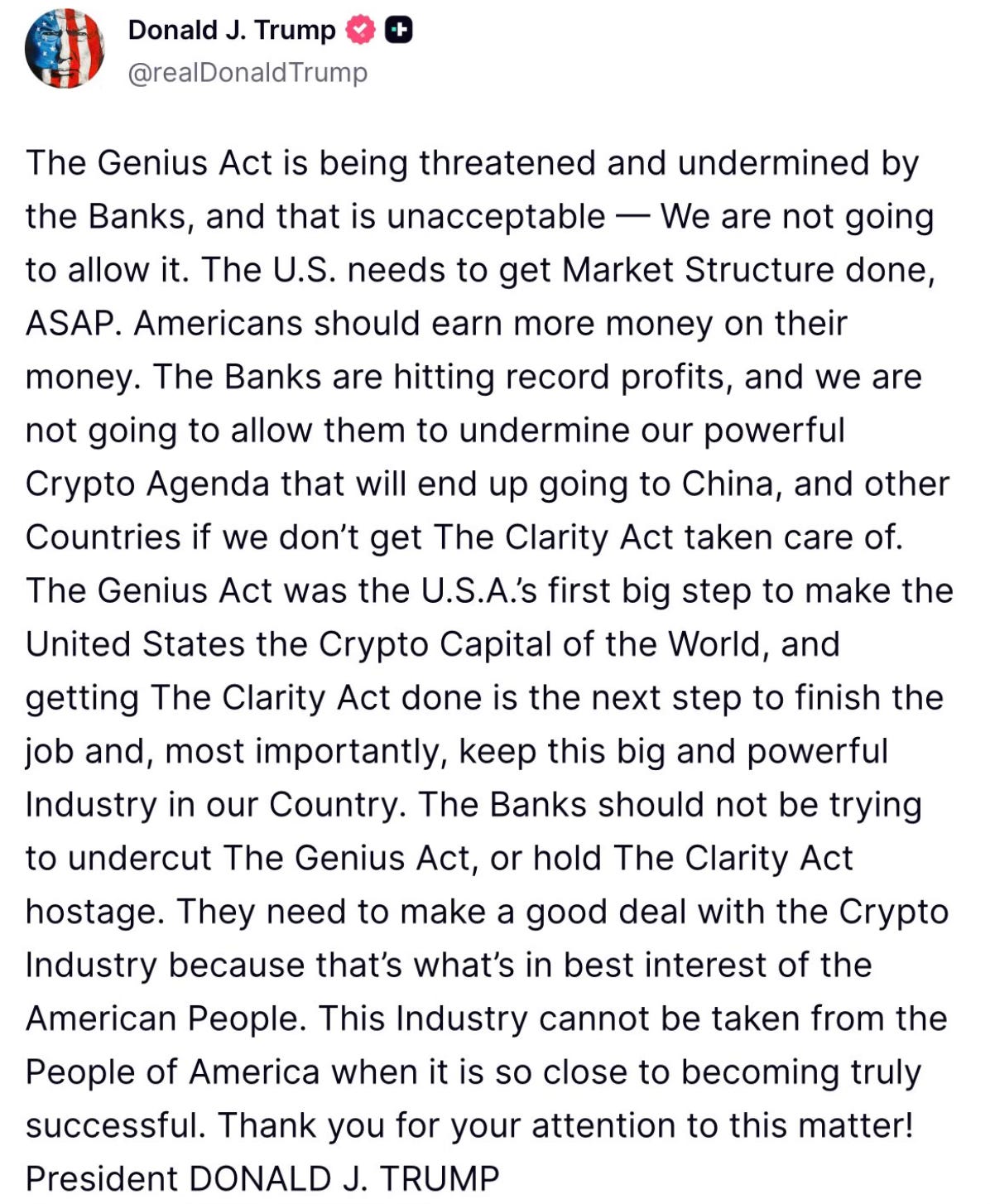

Trump Backs Crypto in Yield Debate After Coinbase CEO Visits White House

In what some in the industry noted as an interestingly timed post given the U.S.’s ongoing military strikes in Iran, President Donald Trump took to Truth Social on Tuesday evening to publicly back the crypto industry in its fight with banks over stablecoin yield, and urge Congress to pass crypto market structure legislation as soon as possible.

Trump’s post follows more than a month of negotiations held by the White House Crypto Council, aimed at helping the crypto industry and banks reach a compromise on allowing crypto companies to offer stablecoin rewards to customers.

The dispute has stalled the Senate Banking Committee from rescheduling a Clarity Act markup, which was postponed after Coinbase CEO Brian Armstrong tweeted in January that he would withdraw support, saying the bill tilted too heavily in the banks’ favor.

After being rebuffed in his attempts to meet with big bank CEOs like Jamie Dimon (JP Morgan) and Charlie Scharf (Wells Fargo) at the World Economic Forum in January, it appears Armstrong has taken his case directly to the President.

Crypto In America reported Tuesday night that a Coinbase delegation visited the White House on Tuesday afternoon to meet Trump, though we could not confirm whether Armstrong met with him personally. Politico then confirmed that Trump and Armstrong did meet privately.

Coinbase did not respond to multiple requests for comment.

Details of the meeting remain unclear, but Trump’s post echoed some of Armstrong’s signature talking points: banks are undermining crypto legislation, and Americans should be able to “earn more money on their money,” — aka earn yield on their savings.

The President’s post hasn’t changed banks’ concerns that vague legislative language could let crypto firms skirt an agreement not to offer yield on idle balances, a banking source involved in the negotiations told Crypto In America.

“We want to continue negotiating, and what we’re trying to do is defend the agreement in-principle of no interest on balances, making sure no holes are punched in that,” the source said, noting they hadn’t heard back from the White House since banks had sent suggestions for legislative text several days earlier.

Trump’s comments follow remarks from JPMorgan CEO Jamie Dimon calling for crypto firms that offer interest on stablecoins to be regulated like banks.

Invest as you spend with the Gemini Credit Card®. Earn up to 4% crypto back on every purchase with no annual fee.

Gemini-branded credit products are issued by WebBank. This is not investment advice and trading crypto involves risk. See Rates & Fees.

The First Fully Licensed Platform for Tokenized Securities: SOMA Talks to Crypto In America

This week on the Crypto In America podcast, Jacquelyn and Eleanor sat down with Will Corkin, co-founder and COO of SOMA.Finance.

Corkin walked us through his decade-plus journey in crypto, from early Security Token Offerings (STOs) to co-founding DeFi platform MANTRA. The conversation dove into the lessons Corkin learned from MANTRA’s $5B crash, the creation of SOMA, and the challenges of building a platform that is fully licensed to tokenize and trade a broad range of securities.

Will explained what makes SOMA different: a non-custodial, decentralized platform where retail and institutional investors, both in the U.S. and overseas, can buy and sell securities on-chain, from listed stocks and bonds to private placements.

He also shared a behind-the-scenes look at the license approval process, how SOMA became the first broker-dealer to operate this kind of platform, and why pre-IPO shares could be the next big driver of crypto adoption.

Watch this episode on all platforms here.

Midweek Recap

ICYMI: Here are some of the biggest stories making headlines this week.

CFTC Chairman Michael Selig plans to approve crypto perpetual futures within the next month as well as write rules and issue guidance for prediction markets.

President Trump urged Congress to pass the Clarity Act, and criticized banks for “threatening and undermining the GENIUS Act.”

Indiana’s Governor Mike Braun signed a bill into law allowing digital assets to be used in certain state retirement plans.

Tether tapped U.S. accounting giant Deloitte for its first USAT reserve report, which showed $17.6 million in reserve assets backing 17.5 million tokens.

The Senate Banking Committee’s 21st Century ROAD to Housing Act includes a provision banning the Federal Reserve from issuing a retail central bank digital currency, though the ban expires in 2030.

Uniswap won full dismissal of the ‘scam token’ class action lawsuit, with the judge ruling the platform cannot be held liable for third-party token issuers’ misconduct.

JPMorgan CEO Jamie Dimon said stablecoin issuers that pay interest on customer balances should be regulated like banks, and should meet capital, liquidity and deposit insurance requirements.

Remember, new editions of the Crypto In America newsletter drop every Monday and Wednesday.

If you like what you’re reading, don’t forget to subscribe!